Direct Answer

The global resistor and capacitor market in 2026 is no longer a stable commodity environment. Instead, it is a segmented supply chain system where demand is heavily influenced by AI infrastructure, automotive electronics, and high-reliability industrial applications.

While standard resistors remain relatively stable, high-spec capacitors—especially MLCCs—face persistent lead-time pressure and allocation constraints, with some reports indicating extended delivery cycles beyond 20 weeks in high-end segments .

This creates a structural shift: the bottleneck in PCB and PCBA production is increasingly determined not by manufacturing capability, but by component-grade availability and BOM engineering quality.

This analysis reflects engineering and production observations from PCB/PCBA manufacturing workflows at Guangzhou Huachuang Precision Technology (HCJMPCBA).

3 Key Takeaways

1. Passive components are now application-driven, not commodity-driven

Resistors and capacitors—especially MLCCs—are increasingly allocated based on application priority (AI servers, automotive, industrial systems).

2. Supply chain risk is shifting upstream to BOM design

Production delays are often caused by:

- missing alternates

- incorrect MPN selection

- lifecycle mismatch (EOL/NRND parts)

3. Manufacturing stability depends on engineering discipline, not procurement speed

Companies with strong BOM control, revision management, and traceability systems experience significantly fewer production interruptions.

1. Global Market Reality: Passive Components Are No Longer Uniform

Historically, resistors and capacitors were considered low-risk passive components with stable pricing and short lead times.

In 2026, this assumption is no longer valid.

Industry data shows that the passive component market is growing rapidly, projected to exceed $48 billion globally in 2026, driven by EVs, AI servers, and high-density electronics systems .

However, growth is uneven:

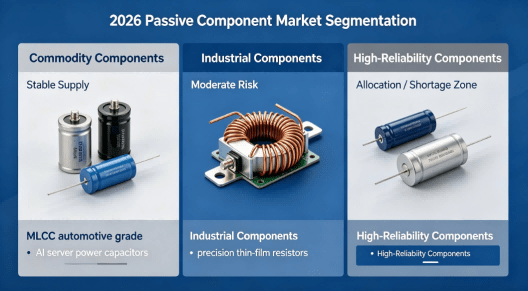

Commodity segment (stable)

- general resistors

- standard capacitors

- low-voltage applications

High-spec segment (volatile)

- automotive MLCCs

- high-frequency capacitors

- precision resistors

- power management capacitors

A key structural change is the emergence of a “K-shaped MLCC market”, where high-end demand diverges significantly from commodity demand.

2026 Passive Component Market Segmentation

2. Why Resistors and Capacitors Are Under Structural Pressure

2.1 AI Infrastructure Demand Explosion

AI servers require significantly higher passive component density compared to traditional systems.

Each AI computing board may contain:

- thousands of MLCCs

- dense decoupling networks

- multi-stage power regulation

A single AI server may use up to 10× more MLCCs than conventional servers .

This demand directly impacts:

- high-capacitance MLCC availability

- low-ESR capacitor allocation

- RF-grade passive components

2.2 Automotive Electronics Expansion

Electric vehicles and ADAS systems require:

- high-temperature capacitors

- vibration-resistant resistors

- safety-certified components

This shifts production capacity away from general electronics.

2.3 Raw Material Sensitivity

Passive components are highly sensitive to:

- silver paste cost

- nickel electrode supply

- copper volatility

- dielectric material constraints

Even minor fluctuations propagate into global pricing adjustments.

2.4 Fragmented Manufacturing Ecosystem

Unlike semiconductors, passive components are:

- highly fragmented

- distributed across multiple regions

- dependent on application-specific production lines

This limits the ability to rapidly increase global capacity.

From a production engineering perspective, the biggest risks are not manufacturing defects but input instability.

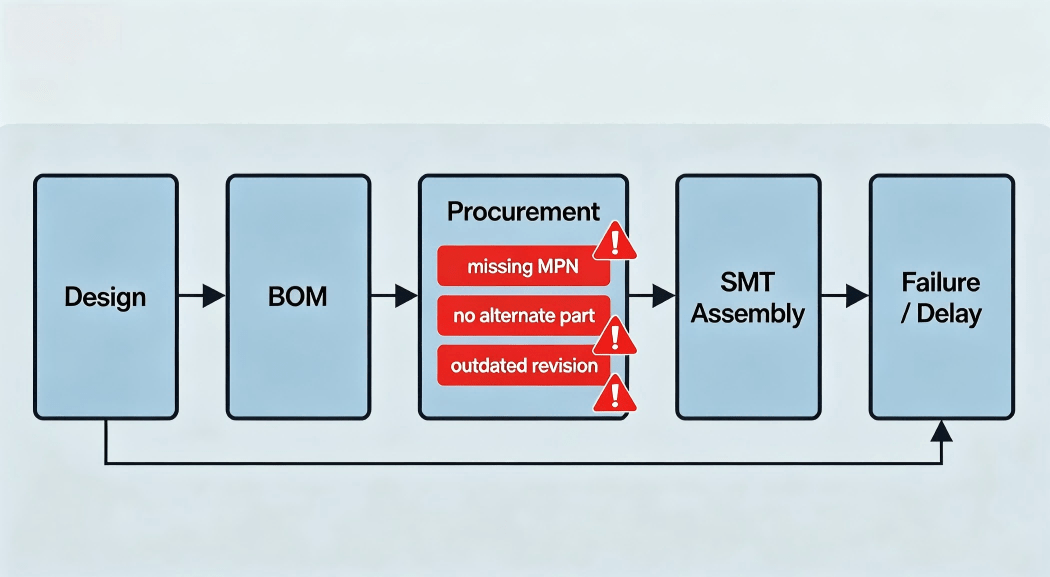

3.1 BOM Instability

Uncontrolled BOMs lead to:

- incorrect procurement

- missing alternates

- outdated revisions entering production

3.2 Substitution Risk

Even “equivalent” components may differ in:

- ESR performance

- temperature characteristics

- tolerance behavior

- footprint compatibility

3.3 Lifecycle Blind Spots

Many components silently enter:

- EOL (End of Life)

- NRND (Not Recommended for New Design)

without immediate visibility in procurement systems.

Bom Driven Failure Chain In Pcba Production

4. Engineering-Level Risk Control in Manufacturing

In structured PCB/PCBA systems like HCJMPCBA, risk control is not handled only at procurement level.

It is embedded into engineering workflow.

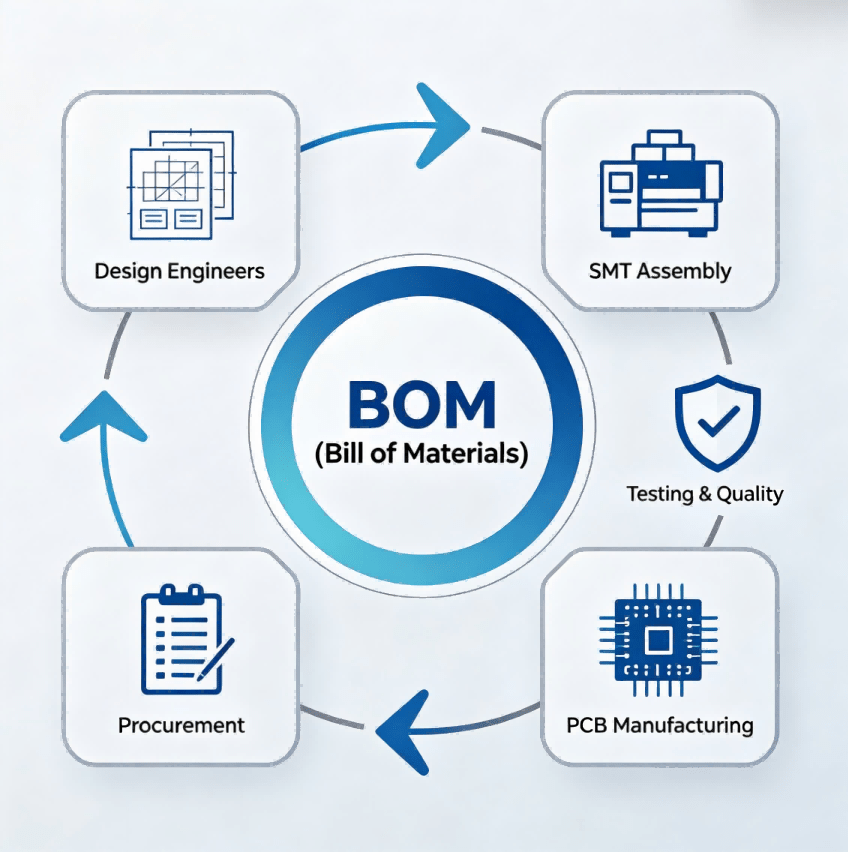

4.1 BOM Engineering Validation

Each BOM is reviewed for:

- MPN accuracy

- lifecycle status

- alternates availability

- footprint compatibility

- compliance requirements (RoHS / REACH)

4.2 Revision-Control System

Production materials are controlled via:

- method numbering

- revision tracking

- change history records

This ensures production consistency across batches.

4.3 Sample Plan & Process Validation

Before mass production:

- controlled sample builds

- inspection sampling plans

- test condition definition

- defect data collection

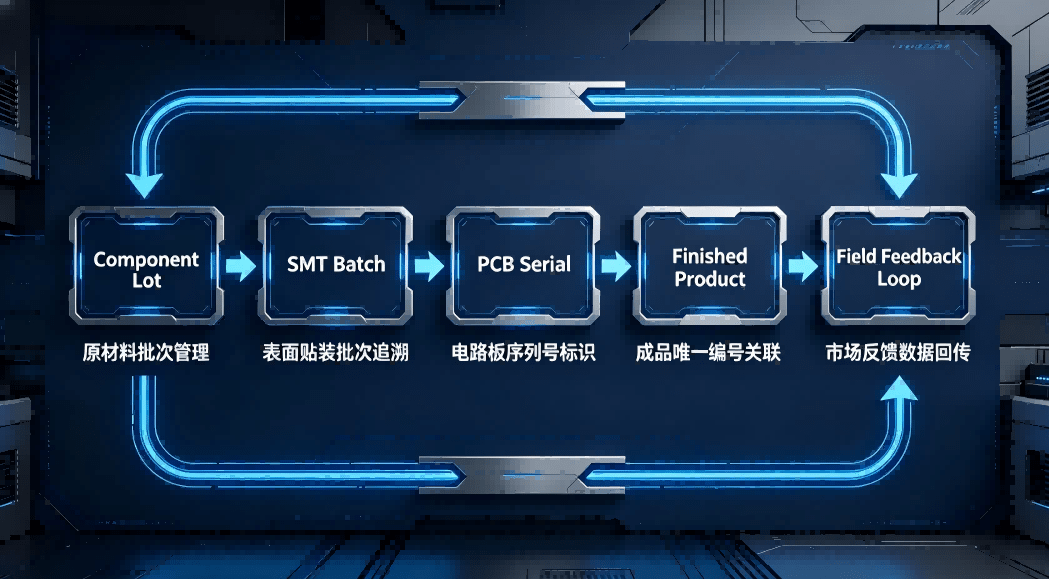

4.4 Traceability System (Lot / Batch / Serial)

Manufacturing traceability includes:

- component lot tracking

- PCB batch identification

- assembly serial linkage

- test result association

This enables root-cause analysis when field issues occur.

Full Traceability Chain In Pcba Manufacturing

5. What Engineering and Procurement Teams Should Focus On

5.1 Lifecycle stability over unit price

Low-cost components often carry hidden supply risks.

5.2 Always define alternate BOM strategy

A robust BOM includes:

- primary MPN

- secondary source

- qualified substitution

5.3 Validate component grades early

Critical parameters include:

- capacitor ESR

- voltage derating

- resistor temperature coefficient

5.4 Treat BOM as a controlled engineering document

Not a static spreadsheet.

6. Industry Observation from Manufacturing Practice

In real PCBA production environments, most delays are caused by:

- BOM inconsistency

- late engineering changes

- unavailable component variants

- incorrect revision control

Not by SMT or PCB fabrication capability.

This reflects a shift in manufacturing reality:

👉 production stability now depends more on upstream data integrity than factory equipment.

7. Decision Table: Component Strategy by Project Type

| Project Type |

Component Strategy |

Risk Level |

| Prototype |

Flexible sourcing |

Medium |

| NPI Stage |

Controlled BOM + alternates |

Medium-High |

| Mass Production |

Locked BOM + AVL |

Low |

| Automotive / Industrial |

Fully traceable BOM |

Very Low |

8. Evidence That OEM Buyers Should Request

To reduce supply chain risk, a capable PCBA supplier should provide:

- BOM revision history

- component sourcing records

- inspection reports

- sample validation data

- traceability mapping (lot → product)

- test condition documentation

- raw production data

These documents reflect process control maturity.

9. Conclusion

The global resistor and capacitor market in 2026 is defined not by uniform shortage, but by segmented availability and application-driven allocation.

The most critical shift is not in component pricing—but in engineering responsibility shifting upstream into BOM design and revision control.

For PCB and PCBA manufacturing, long-term stability depends on:

- BOM discipline

- lifecycle awareness

- traceability systems

- structured validation processes

Manufacturing success is increasingly determined before production begins—at the BOM and engineering review stage.

CTA

For more information about PCBA services, please contact Guangzhou Huachuang Precision Technology(HCJMPCBA).

Update triggers: standard revision changes / recurring questions / production checklist updates.